In Search of Missing Fortunes

"Time in the market is more important than timing the market."

Greetings longtime readers! In spite of what you might have seen on the news regarding Mexico, all is well here in San Luis Potosi where I'm currently living. I'm enjoying retirement by filling my days with exercise, good meals, naps, and an overall relaxed lifestyle. At this point, I can't ever imagine returning to a "normal" job!

In this post, I want to take a look at two programs my wife and I have participated in for over 45 years: Social Security and Medicare.

Twelve years ago when I turned 50, I realized that Zena and I had made significant contributions to both plans over the years. Naturally, this led to the creation of a spreadsheet to determine 1.) our total contributions and 2.) the present value (PV) of our contributions had they been invested in a basic and boring S&P 500 index fund.

Analyzing our S.S. contributions made me wonder...

What If Social Security Worked Like an IRA?

Now, before I go any further, this post isn't going to be an attack on the United States Social Security Administration and its shortcomings. Instead, this will be a thought experiment to illustrate the power of steady investment contributions over decades. After all, S.S. contributions are taken out of workers' paychecks throughout their working years regardless of how they feel about the program.

According to the SSA website, S.S. is a mandatory "federal social insurance program designed to provide a foundational source of income for retirees, disabled workers, and the families of deceased workers. In other words, S.S. is NOT a full-on retirement plan like an IRA or a 401k.

One of the main benefits of IRAs is that their contributions can be invested in many growth vehicles such as stocks bonds, mutual funds, and ETFs. Another benefit is that upon the death of the account holder, the remaining IRA balance can be left to heirs. There are no such provisions with the S.S. plan.

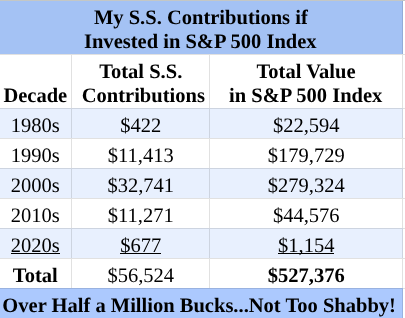

Nevertheless, let's pretend that the S.S. plan functioned like an IRA. To get some numbers I put my annual S.S. contributions into Grok.com and requested 1.) my total S.S. contributions by decade, and 2.) the total value of these contributions had they been invested in an S&P 500 index fund. Here are the totals by decade as of March of 2026:

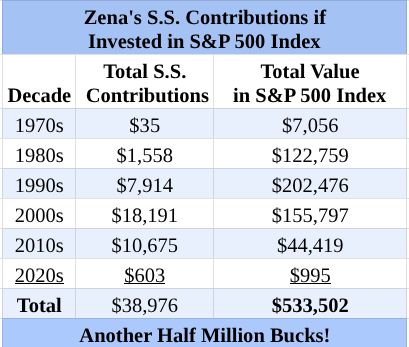

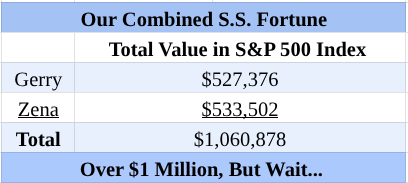

Wow, an extra $527k of retirement savings sure would be nice, wouldn't it? Oh well, there's no need to cry over missing fortunes. Next, I put my wife's S.S. contribution numbers into Grok and requested the same info; here are her numbers:

Once again, another mythical balance of over $500k appeared. It's interesting to note that my wife's balance was greater than my balance by $6k ($533k - $527k) in spite of the fact that I contributed $18k ($57k - 39k) more to the plan. That just goes to show that investing early allows your investments to grow for a longer time span.

For example, her $35 of contributions in the 1970s would have grown to over $7k! While that may sound impossible to many people, that growth only represents a 12% annual return over the 47-year time horizon. "Time in the market" matters!

Now, let's combine our totals and see how much our imaginary S.S. IRA plan would be worth:

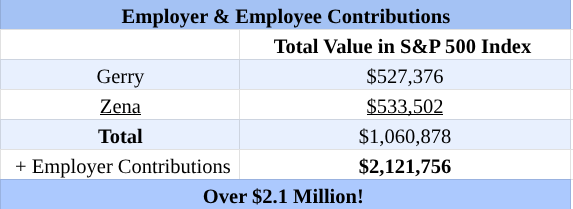

Ouch, I can't lie, it hurts to see that we're "missing" over $1 million from "our" accounts, but the situation is even worse. Why? Simple, because the balances above only show our S.S. contributions; however, they do not include our employers' contributions over the decades.

Do see where I'm going with this? In order to get an accurate view of our S.S. IRA balances, we should double the amounts above. Why? Because both the employee and the employer contribute 6.2% to S.S.; that's a grand total of 12.4% to the plan.

Here are our balances adjusted (doubled) to include our employers' S.S. contributions over the years:

Total Missing Fortune = $2,121,756!

Okay, let me regain my composure...😢

Instead of lamenting our missing sum of $2.1 million, let's focus on the fact that over our working lives our S.S. contributions of only $95k ($56k + $39k) would have grown to an astounding final amount. (At least they did in this fictitious thought experiment. 😉)

Now, on to Medicare!

What if Medicare Worked Like an HSA?

Next, let's assume that over the years our Medicare contributions were deposited in an account similar to a health savings account (HSA). Let's also assume that all Medicare contributions were invested in an S&P 500 index fund.

In case you don't know, Medicare is a federal health insurance program for people aged 65 and older. It consists of four parts (A-D): Hospital Insurance, Medical Insurance, Medicare Advantage Plans, and Prescription Drug Coverage. (more Medicare info here)

An HSA is a tax-advantaged savings account used to pay qualified medical expenses. In the "real" world, HSA contributions are tax-deductible, grow tax-free, and withdrawals for qualified medical expenses are also tax-free. In order to open an HSA account, individuals must have a high-deductible healthcare plan (HDHP). (more HSA info here)

In 2013 we began using a HDHP, and we opened an HSA account at Fidelity. As a result, we now have over $140k that we can use to cover our future qualified medical expenses.

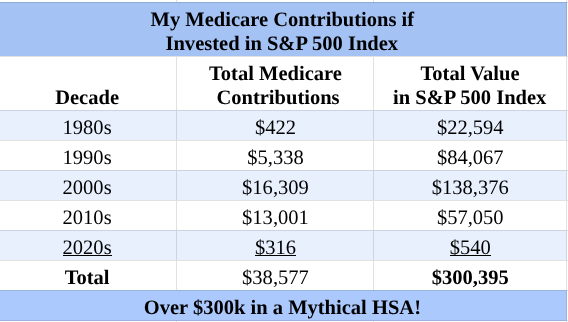

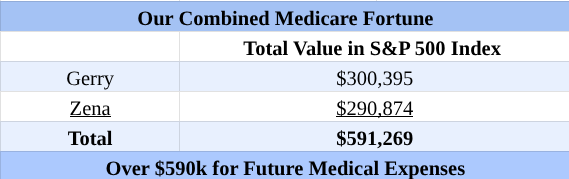

Now, let's see how much my Medicare contributions would total had they been invested. The numbers below include my contributions of 1.45% and my employers' contributions of 1.45%:

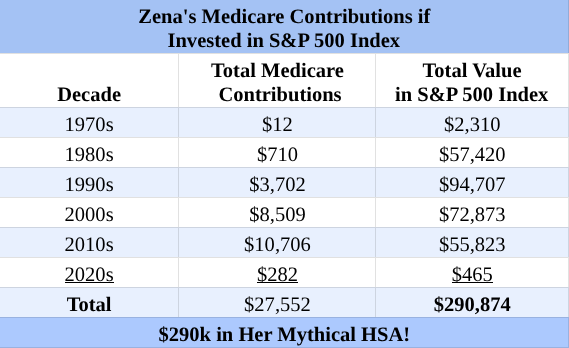

Without a doubt, an extra $300k in my HSA would be incredible, but that will never happen. Let's take a look at Zena's Medicare contributions:

What can I say? That would've been a lot of HSA money! Here's how much our Medicare HSA could have been:

A little shy of $600k for future medical expenses...😪

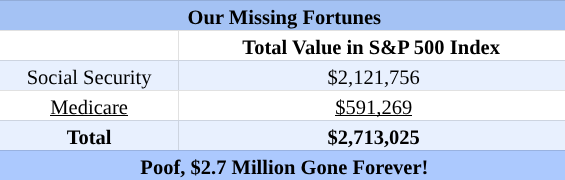

Grand Total of Our Missing Fortunes

Here's what our accounts are worth in a parallel financial universe:

There you have it: $2.7 million...POOF!

Final Thoughts

What can we take away from this post?

- Our hypothetical missing fortunes are the results of consistent contributions over four decades. Social Security (6.2%) and Medicare (1.45%) contributions were only 7.65% of our paychecks. Plus, our employers contributed an equal amount to the programs resulting in combined contributions of 15.3%. Imagine if everyone saved 15% of their paycheck from ages 18 to 62. Saving and investing in a basic and boring S&P 500 index fund could generate a solid retirement nest egg.

- Government programs such as Social Security and Medicare exist to provide a financial and medical safety net for all of the nation's inhabitants. They were never designed to be wealth-building accounts, and that's okay.

- If you feel that Social Security and Medicare are unfair and outdated programs, it's time for you to "stick it to the man" and blow them out of the water. How? Simple, fully fund all of your accounts: HSA, IRA, 401k/403b, 457, and brokerage accounts. That will show Uncle Sam that no bad government plan will ever keep you down!

If you made it this far, thanks for reading! I hope this post helped you understand the value of being in the stock market over a long period of time. As they say, "Time in the market is more important than timing the market." Now, go forth and hammer your FI plan!

Best of luck to all,

GB