My Trillionaire Plan Revisited

"Wow, if this is financial failure, keep it coming!"

Hello readers, today's post takes us back to 2015 when I had a crazy question:

"Would it be possible FOR ME to become a trillionaire? If so, how?"

After all, someone had to give Elon, Zuck, Warren, and the Bez a run for their money. So, I wrote a post that hit the FIREsphere bullseye when it was featured at RockStarFinance.com (RIP and greetings J$!).

Trillionaires Aren't a Dime a Dozen!

While the post was a success, it passed into the cyber-ether when I moved my blog from Wordpress to Ghost.io 😢. Check out the photo below; it was taken by my buddy Freddy Sublett ✌️.

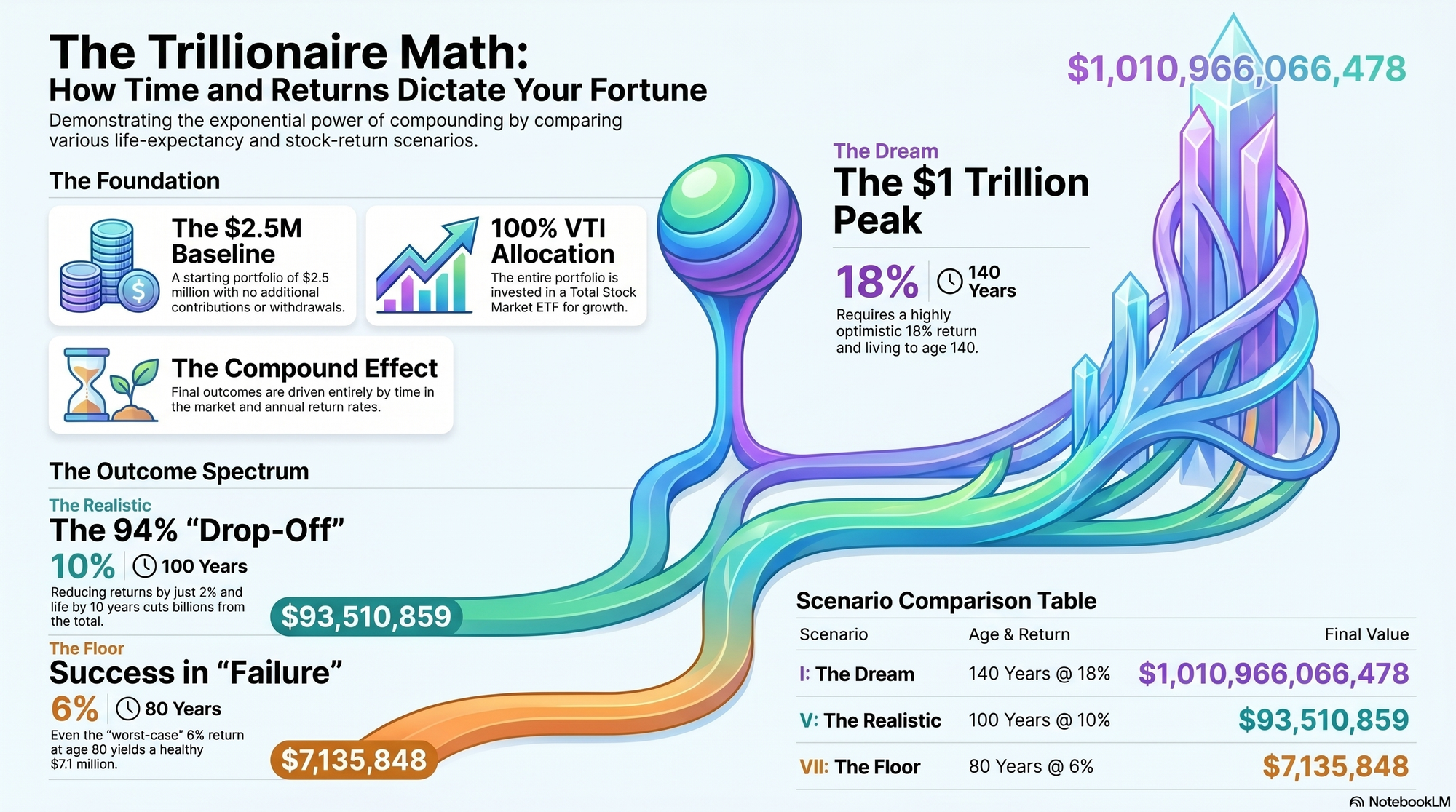

Dry your tears because in today's post we'll revisit My Trillionaire Plan to evaluate seven financial scenarios.

Each scenario will become less optimistic and more realistic; both life expectancy and expected return will be declining.

However, before we proceed we need to make a few financial assumptions regarding a.) present value (PV) and b.) payments (PMT).

Financial Assumptions

If you've read "Our Story," you already know where we stand financially. For this financial experiment, we'll assume a starting value (PV) of $2.5 million.

We'll also assume that we won't be adding to nor taking from the portfolio and its growth, so the PMT will be $0. (After all, we now have two pensions and one Social Security check. 😉)

- Present Value (PV) = $2,500,000

- Payment (PMT) = $0

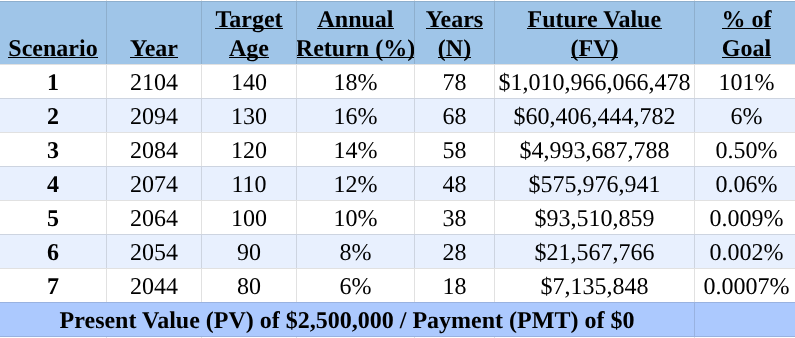

It's also important to note that I am currently 62 years old. Therefore, the number of time periods (N) for my fortune to grow will be limited by my advanced age. Also, the expected return (I / %) will vary from super aggressive to depressingly conservative (from 18% down to 6%).

Finally, 99% of my portfolio will be invested in Vanguard's VTI, a basic total stock market ETF. Now let's look at the first scenario:

Scenario I: Living to 140 with 18% Return

Obviously, this scenario is highly optimistic because it assumes that I'll live another 78 years and my portfolio will enjoy an 18% return over that time period.

(I know what you're thinking ladies: ancient, handsome, and loaded...back off and keep your hands to yourselves!)

If my diet-and-exercise program pays off, the advanced age of 140 is a guaranteed certainty! Plus, my portfolio will go on an extended bull run as AI and future technological developments push the stock market into the stratosphere. It's. Gonna. Be. EPIC!

Future Value in 2104 =

$1,010,966, 066,478!

Wow, a trillion bucks! Nonetheless, I can hear the Doom Patrol in the back saying:

Okay Big Boy, cool your jets and slow your roll because your assumptions are WILDLY optimistic.

Maybe so since we never know what the future holds. Now, let's knock off 10 years from my life expectancy and reduce my portfolio's expected return by 2%. (We'll be doing the same in every scenario going forward.)

Scenario II: Living to 130 with 16% Return

Now, what happens if I only live 68 more years and earn a return of "only" 16%.

Future Value in 2094 =

$60,406,444,782

Not bad, but $60 billion is still considerably less than $1 trillion; 94% less to be exact. That extra 2% return (18% vs 16%) and the additional 10 years of compounding (78 years vs 68 years) made a HUGE difference. Never underestimate the power of compounding growth over decades! Now, let's move on.

Scenario III: Living to 120 with 14% Return

Finally, we're starting to get a whiff of reality. The age of 120 is below the world record of 122 (👏 to Jeanne Calment). Plus, 14% is a really good return, but it wouldn't win me any bragging rights on Wall Street. (However, I do acknowledge that 14% over a 58-year span would be incredible. 🔥) Let's check the result:

Future Value in 2084 =

$4,993,687,788

I hate to sound like an ingrate, but $5 billion sure isn't $1 trillion! Once again, time in the market and investment return make a big difference on the bottom line. Nevertheless, being a multi-billionaire wouldn't be the worst thing that ever happened to me and my family. 😄

Scenario IV: Living to 110 with 12% Return

Living to 110 is not unheard of, and earning a 12% return is also within the realm of possibility. But, those are still some pretty hefty numbers. Let's see what this scenario yields:

Future Value in 2074 =

$575,976,941

Just shy of $600 million which is a far cry from a trillion bucks, but you'll hear no complaints from me. As always, a shorter investment frame and a lower investment return result in a lower future value. No big surprise here.

Scenario V: Living to 100 with 10% Return

Since longevity is sure to increase due to upcoming medical innovations, becoming a centenarian shouldn't be that big of a deal. (After all, I'm not a vegan and I'm unvaxxed 😜.) Earning 10% in the stock market isn't guaranteed, but it's not a crazy expectation, is it? Let's see the results:

Future Value in 2064 =

$93,510,859

Over $90 million! Wow, if this is financial failure, keep it coming! On to the next scenario...

Scenario VI: Living to 90 with 8% Return

This scenario is more grounded in biological and financial reality. People live to 90 all the time, and an 8% stock market return would be considered unspectacular.

Future Value in 2054 =

$21,567,766!

A final sum of over $21 million, while light years from $1 trillion, would be generational wealth for my heirs. Now for the last scenario:

Scenario VII: Living to 80 with 6% Return

Barring an unforeseen health problem or accident, this scenario is my worst case scenario. Longevity seems to run in my family even among individuals who pay no attention to their health. (You know who you are. 😉) A 6% stock market return would be a bummer after so many years of double-digit returns. Let's take a look at this hyper-crappy scenario:

Future Value in 2044 =

$7,135,848!

Yikes, this lands many time zones away from my intended goal of $1 trillion. That said, I don't really care! That's much more money than I came into the world with. Knowing that my heirs would be left in a good financial position would give me peace as I entered the celestial realm.

My Trillionaire Plan Revisited Recap

Final Thoughts

Just like my 2015 "My Trillionaire Plan" post illustrated, becoming a trillionaire is possible. However, it's not very probable, and that's A-okay. After all, even the worst scenarios above contain strong 7-figure final values.

If you haven't figured it out yet, the point of this post is to show you, dear reader, the power of compounding over multi-decade time periods. I hope this made you think of the enormous possibilities you have over the course of your (hopefully long) lifetime.

Ancient, Handsome, and Loaded!

Which scenario is most likely for you? Why? I think scenario VI is most likely for me, and with a little luck I might make it to scenario V. Wish me luck!

Trillionairely Yours,

GB